When my mother could no longer live alone, I assumed Medicare would pay for her nursing home care. She had worked her whole life. She had paid her taxes. She was entitled to this, right? I was wrong. The morning I sat down with the admissions coordinator and learned that Medicare would not cover her long-term stay was one of the most stressful moments of my life. I had to scramble to figure out how to pay for her care while she was already settling into her new room.

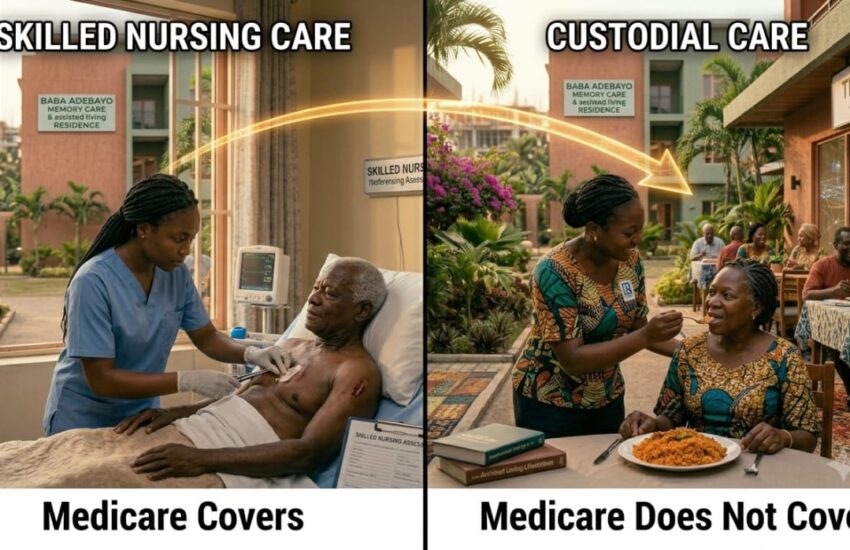

Medicare generally does not pay for long-term nursing home stays or custodial care . Custodial care is the nonmedical help with activities of daily living like bathing, dressing, eating, and toileting . This is the type of care most people need in a nursing home, and Medicare explicitly excludes it from coverage .

What Medicare will pay for is short-term, medically necessary skilled nursing care in a skilled nursing facility after a qualifying hospital stay . This is a critical distinction. A nursing home mostly provides long-term custodial care. A skilled nursing facility offers short-term professional medical care for people recovering from surgery or an acute health condition .

To qualify for a Medicare-covered skilled nursing facility stay, your loved one must meet specific criteria. They must have been formally admitted as an inpatient to a hospital for at least three consecutive days . The day they enter the hospital counts, but the day they are discharged does not .

Time spent in the emergency room or under observation status does not count toward the three-day requirement . They must enter a Medicare-certified skilled nursing facility within 30 days of leaving the hospital, and they must need daily skilled nursing care or skilled therapy services for a condition that was treated during the hospital stay .

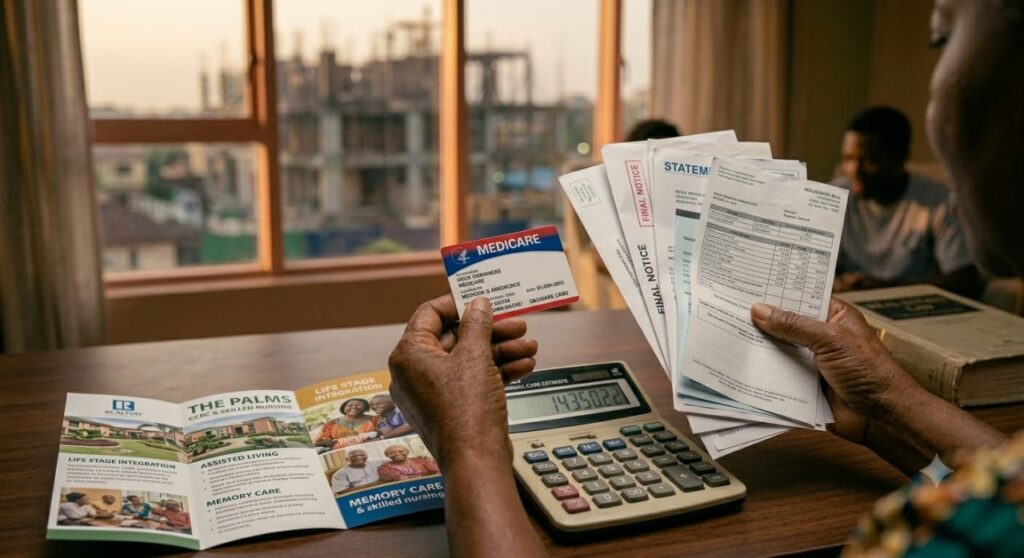

If your loved one meets all these requirements, Medicare Part A covers the full cost of the first 20 days in a skilled nursing facility . For days 21 through 100, Medicare covers part of the cost, and you are responsible for a daily coinsurance payment. In 2026, that coinsurance is $217 per day . After day 100, Medicare stops paying entirely, and you are responsible for 100% of the cost . The median cost of a nursing home room with a semi-private room is around $9,581 per month, and a private room averages $10,798 per month .

Many families mistakenly expect Medicare to cover long-term care, and it can be devastating to discover otherwise when it is already needed . Colleen Duewel, an eldercare specialist, confirms, “Medicaid helps with the long-term care portion (custodial care), while Medicare continues to manage the individual’s medical health” .

Medicare can also help pay for other health care costs while your loved one is in a long-term nursing home, even if it won’t cover the stay itself. Doctor visits, durable medical equipment like wheelchairs, prescription medications, and preventive services may still be covered . It just will not cover the room, board, and daily assistance with activities of daily living.

Since Medicare does not cover long-term care, you need other ways to pay. Medicaid is the country’s largest payer of long-term care services and will pay for nursing home care for those who meet income and asset requirements . About 62% of nursing home residents rely on Medicaid . Another option is long-term care insurance, which you should ideally purchase in your 50s when premiums are lower .

Veterans may qualify for benefits through the VA. Some Medicare Advantage plans offer some benefits, but they vary widely. Gretchen Jacobson, vice president of the Medicare program for the Commonwealth Fund, notes, “Medicare Advantage does not have the consistent benefits original Medicare does”. I wish I had known all of this long before my mother needed care. I would have planned differently. I would have looked into long-term care insurance. I would have understood the difference between skilled care and custodial care. I would have known what questions to ask.

If you are facing this situation, start by planning early. Talk to a financial planner. Research long-term care insurance. Understand your state’s Medicaid rules. And when you are considering a facility, ask if it is Medicare-certified and what your loved one’s coverage will actually include. There is so much more to learn about paying for long-term care. Our website is filled with articles on Medicare, Medicaid, and financial planning for senior care. Head over and explore, because knowing the rules before you need them can save you from a crisis.

References

Medicare. (n.d.). *Nursing home care*. https://www.medicare.gov/coverage/nursing-home-care

Medicare. (n.d.). *Nursing homes*. https://www.medicare.gov/providers-services/original-medicare/nursing-homes

Medicare. (n.d.). *How can I pay for nursing home care?* https://www.medicare.gov/providers-services/original-medicare/nursing-homes/payment

National Council on Aging. (2026, January 6). *Does Medicare pay for nursing homes?* https://www.ncoa.org/article/does-medicare-cover-nursing-homes-what-older-adults-and-caregivers-should-know/

Solace Health. (2024, November 19). *What happens when Medicare stops paying for nursing home care*. https://www.solace.health/articles/medicare-stops-paying-for-nursing-home-care